In the insurance industry’s dynamic environment, where data-driven decisions and tailored experiences are crucial, there’s a pressing demand for innovation. Insurance companies are grappling with myriad challenges, from meeting customer expectations to optimizing operational efficiency. The emergence of AI is a game-changer.

AI enables insurance providers to personalize policies, fine-tune pricing strategies, and streamline processes with precision. Using advanced machine learning models, insurers can automate tasks and enhance operational efficiency. Building enterprise AI solutions for insurance enables insurers to mitigate risk more effectively and to deliver unparalleled customer experiences that set them apart from the competition.

But that’s not all. Enterprise AI solutions also empower insurers to generate fresh insights from synthetic data, enabling faster and more informed decision-making. Whether it’s predicting claim outcomes or identifying potential fraud, the possibilities are endless with enterprise AI solutions for insurance.

So, as the insurance industry braces itself for tomorrow’s challenges, one thing is clear: building enterprise AI solutions for finance is not just a tool—it’s a strategic imperative, driving innovation, efficiency, and customer satisfaction in equal measure.

This article explores the profound impact of artificial intelligence on the insurance sector and delves into building enterprise AI solutions tailored specifically for insurance.

- Understanding AI’s impact on the insurance industry

- AI-enhanced customer and business lifecycle management in insurance

- Use cases of AI in insurance

- Types of models used in building enterprise AI solutions for insurance

- How to build enterprise AI solutions for insurance operations?

- Benefits of implementing enterprise AI solutions in insurance workflow

- How does LeewayHertz aid in integrating AI solutions into your insurance workflow?

- Ensuring trust: Ethical considerations and compliance in insurance practices

Understanding AI’s impact on the insurance industry

AI solutions are transforming the landscape of insurance businesses, offering many advantages across various operations. Through sophisticated algorithms, these solutions analyze vast troves of data, improving precise risk assessment and underwriting processes. This accuracy not only aids in better pricing policies but also ensures that insurance providers can effectively manage their risk portfolios.

In insurance claims processing, AI streamlines workflows by automating repetitive tasks and detecting fraudulent activities more efficiently. This expedites the settlement process and helps minimize losses due to fraudulent claims. Additionally, AI-powered insurance chatbots offer personalized customer service around the clock, enhancing customer engagement and satisfaction.

Moreover, predictive analytics enables insurers to anticipate market shifts, customer preferences, and emerging risks, empowering them to make proactive decisions and tailor products to meet evolving demands. By enhancing operational efficiency, reducing costs, and fostering innovation, enterprise AI solutions enable insurance companies to maintain competitiveness in a dynamic industry while delivering exceptional customer experiences.

AI-enhanced customer and business lifecycle management in insurance

AI in insurance customer lifecycle management

Incorporating AI into insurance organizations transforms each phase of the customer lifecycle, from awareness to post-purchase engagement, by providing data-driven insights and personalized experiences.

Awareness phase:

- Market segmentation: AI analyzes consumer data to segment the insurance market. By pinpointing crucial demographics, behaviors, and preferences specific to insurance consumers, AI enables precise targeting of specific groups with tailored insurance products. This data-driven methodology elevates marketing strategies, ensuring that promotional endeavors are finely attuned to prospective policyholders’ specific needs and preferences within the insurance landscape.

- Personalized marketing: AI-driven algorithms meticulously analyze individual customer profiles and behaviors in the insurance sector. By understanding factors such as life stages, financial status, and past interactions with insurance products, these algorithms craft personalized marketing messages tailored to address specific insurance needs and concerns. This ensures that promotional efforts resonate deeply with potential policyholders, offering relevant solutions and fostering a stronger connection between insurers and their target audience.

- Content recommendations: AI utilizes sophisticated algorithms to analyze customer profiles and behaviors, enabling insurance companies to suggest educational content tailored to individual interests and needs. This content includes articles, videos, or webinars designed to explain various insurance products’ importance and benefits. By addressing specific concerns or misconceptions and providing relevant information, AI-driven recommendations empower potential customers to make informed decisions about insurance coverage, thereby increasing their understanding of its value in mitigating risks and protecting their financial well-being.

Consideration phase:

- Risk assessment: AI assesses individual risk profiles in the insurance sector. It analyzes diverse data points such as demographics, health records, lifestyle factors, and previous insurance claims history, providing insurers with comprehensive insights into each customer’s risk profile. This enables insurance companies to determine appropriate coverage options and pricing strategies tailored to each policyholder’s specific needs and circumstances. Ultimately, AI-driven risk assessment enhances underwriting accuracy, ensures fair pricing, and optimizes insurance coverage for customers.

- Policy customization: AI-driven tools allow customers to customize their policies to their needs. By leveraging these tools, policyholders can select coverage levels, deductibles, and additional features that best align with their specific circumstances, risk tolerance, and financial goals. The personalized approach ensures that customers receive insurance coverage that adequately protects their assets and meets their unique needs, enhancing satisfaction and peace of mind.

- Real-time quotes: Using AI, insurance companies can swiftly generate real-time insurance quotes tailored to customers’ needs. AI algorithms instantly calculate personalized quotes by analyzing customer input, including demographic information, risk factors, and coverage preferences. This empowers customers to compare coverage options and pricing scenarios, enabling them to make well-informed decisions about their insurance policies. Ultimately, this streamlined process enhances transparency and efficiency in insurance purchasing, leading to higher customer satisfaction and engagement.

Purchase phase:

- Streamlined application process: In the insurance sector, AI-driven automation simplifies the application process by seamlessly handling form filling, verifying information accuracy, and offering immediate assistance to applicants. Through real-time data validation and analysis, AI ensures that all required fields are accurately completed and cross-references the provided information with external databases for verification. This streamlined approach minimizes the likelihood of errors and provides instant support to applicants, ultimately reducing friction and dropout rates in the insurance application process.

- Dynamic pricing: AI dynamically modifies insurance premiums by continuously evaluating various factors, such as changes in risk profiles, market dynamics, and individual customer behavior. This real-time adjustment ensures that policyholders receive fair and competitive pricing reflective of their current circumstances. By leveraging AI-driven pricing models, insurance companies can offer personalized premiums that align with each policyholder’s unique risk exposure, enhancing transparency and satisfaction in the pricing process.

- Instant approval: In the insurance sector, AI algorithms quickly and accurately evaluate policy applications. These algorithms swiftly determine policy eligibility by analyzing diverse data sets, including medical history, financial records, and lifestyle factors. This efficiency expedites the approval process and reduces the likelihood of errors, ensuring prompt policy issuance to qualified applicants while minimizing delays and enhancing customer satisfaction.

Post-purchase engagement phase:

- Customer support: AI-driven chatbots provide 24/7 assistance to policyholders. These insurance chatbots address insurance-related inquiries, including coverage details, policy terms, and premium calculations. Moreover, they guide customers through the claims process, offering step-by-step assistance, document submission guidance, and updates on claim status. By providing immediate and accurate support, these chatbots enhance customer satisfaction, streamline interactions, and expedite claims resolution, ultimately improving the overall customer experience within the insurance sector.

- Proactive communication: AI-driven platforms send personalized messages to policyholders, ensuring they remain informed about critical updates. These platforms notify customers about upcoming renewal deadlines, policy changes, and relevant updates specific to their coverage. By delivering tailored communications, insurers enhance customer engagement and loyalty, fostering a sense of trust and satisfaction among policyholders. This proactive approach strengthens the insurer-policyholder relationship, encouraging long-term retention and advocacy within the insurance ecosystem.

- Customer feedback: AI thoroughly analyzes feedback and sentiment, pinpointing areas for enhancement in insurance services. By understanding customer sentiments and addressing their concerns, AI facilitates ongoing improvements in retention strategies, ultimately enhancing the overall customer experience. This customer-centric approach ensures that insurers continuously refine their services to meet evolving needs, fostering greater satisfaction and loyalty among policyholders.

By incorporating AI solutions into each stage of the customer lifecycle, insurance organizations can streamline operations, improve customer experience, and drive growth in a highly competitive market.

Transform Insurance with Enterprise AI!

Unlock the power of enterprise AI solutions with LeewayHertz. Tailored

for insurance, crafted for success.

AI in insurance business lifecycle management

The business lifecycle for the insurance sector typically encompasses several stages, including product development, customer acquisition, underwriting, claims processing, and customer retention. Throughout these stages, AI is crucial in enhancing efficiency, improving decision-making, and delivering personalized experiences. Here’s how AI aids each stage of the insurance business lifecycle:

Product development:

- Market analysis: AI algorithms greatly enhance market analysis in the insurance sector. They analyze extensive datasets to identify opportunities for new or improved insurance products. This analysis helps insurers adapt to evolving customer needs and maintain relevance in a dynamic industry landscape. By leveraging AI insights, insurance companies can develop innovative products that meet customer needs and stand out from competitors.

- Customer insights: AI harnesses customer data in the insurance sector to glean valuable insights into shifting preferences and evolving needs. AI identifies emerging trends and patterns by analyzing demographic information, claims history, and customer interactions, guiding product development decisions. This data-driven approach ensures that insurance companies align their offerings closely with customer expectations, enhancing relevance and competitiveness in the market.

Customer acquisition:

- Targeted marketing: AI empowers insurers to refine their marketing efforts by analyzing demographic data, online behavior, and other relevant factors of potential customers. By leveraging this data, AI algorithms can identify potential customers more likely to require specific insurance products or coverage options. This targeted approach allows companies to tailor marketing campaigns and messages to resonate with the needs and preferences of individual customers, ultimately improving the effectiveness of their marketing initiatives and increasing the likelihood of customer engagement and conversion.

- Lead scoring: In the insurance sector, AI algorithms play a crucial role in lead prioritization by analyzing various data points to determine the likelihood of conversion. By considering factors such as demographic information, previous interactions, and online behavior, AI identifies high-potential prospects most likely to purchase insurance products among the target customer base. This prioritization enables insurers to allocate resources effectively, prioritizing leads with the highest conversion likelihood and ultimately improving overall conversion rates and sales performance.

- Personalized recommendations: AI algorithms analyze customer data to deliver personalized insurance recommendations tailored to individual needs and preferences. By considering demographics, lifestyle, and past interactions, AI can suggest insurance products that align closely with each prospective customer’s unique circumstances. This personalized approach enhances engagement and trust, increasing the chance of conversion as customers feel understood and valued by the insurer.

Underwriting:

- Risk assessment: AI automates risk assessment in the underwriting process by analyzing customer information, historical claims, and other relevant data to evaluate risk factors for each applicant accurately. This streamlined approach not only improves efficiency but also enhances insurers’ profitability and competitiveness in the market.

- Automated underwriting: AI optimizes underwriting workflows by automating manual tasks and offering decision support. By analyzing vast datasets, including applicant information and risk factors, AI algorithms expedite the underwriting process while ensuring consistency and accuracy. This automation reduces processing times, enhances efficiency, and enables insurance companies to make well-informed underwriting decisions, ultimately improving the overall effectiveness of the underwriting process.

- Dynamic pricing: AI facilitates dynamic pricing adjustments by analyzing real-time data, including customer behavior, claims history, and market trends. This enables companies to adapt pricing strategies dynamically, responding promptly to changes in risk profiles and market conditions. By leveraging AI-powered algorithms, companies can optimize pricing to accurately reflect current risk levels, ensuring competitive premiums while maintaining profitability.

Claims processing:

- Fraud detection: AI algorithms scrutinize claims data to uncover patterns suggestive of fraudulent activity, empowering companies to pinpoint and probe suspicious claims more efficiently. By leveraging advanced analytics, AI enhances fraud detection capabilities, enabling swift identification and investigation of potentially fraudulent claims. This proactive approach mitigates financial losses and increases trust in the insurer’s ability to combat fraud effectively.

- Automated settlement: AI streamlines claims settlement processes by automating tasks, reducing manual intervention and processing times, and improving accuracy. This automation enhances customer satisfaction by expediting claim resolutions and ensuring fair outcomes. Insurers can leverage AI to swiftly analyze claims data, detect patterns of fraudulent activity, and mitigate risks effectively. Overall, AI-driven automation transforms claims management, delivering faster, more precise, and customer-centric solutions.

- Claims triage: AI efficiently prioritizes incoming claims by assessing their severity and complexity, ensuring that critical cases receive prompt attention. By automating the triage process, AI optimizes claim handling, leading to faster resolutions and improved customer satisfaction. This streamlined approach enables insurance companies to allocate resources effectively, focusing on resolving high-priority claims while maintaining operational efficiency.

Customer retention:

- Retention strategies: In the insurance sector, AI utilizes sophisticated algorithms to scrutinize customer data, pinpointing potential retention risks and opportunities. By analyzing factors like policy usage, claims history, and customer interactions, AI empowers insurers to craft targeted retention strategies. These strategies may include implementing personalized offers tailored to individual policyholders’ needs or initiating loyalty programs to incentivize continued engagement. This data-driven approach ensures that insurers can proactively address churn risks and foster long-term relationships with their policyholders, ultimately enhancing customer retention and satisfaction.

- Personalized renewal offers: Using sophisticated algorithms, AI scrutinizes customer behavior and policy usage data within the insurance company. By analyzing factors such as claims history, coverage utilization, and interaction patterns, AI identifies opportunities to personalize renewal offers and incentives. This tailored approach increases the likelihood of policyholders renewing their insurance policies, fostering higher retention rates and boosting overall customer satisfaction within the insurance organization.

- Automated renewal process: AI streamlines the insurance policy renewal process by automating key tasks such as sending renewal reminders, generating personalized renewal quotes, and facilitating seamless payment processing. This automation ensures that policyholders are promptly notified of upcoming renewals and provided with competitive pricing options tailored to their needs. By reducing administrative burden and simplifying the renewal process, AI helps minimize churn rates and ensures uninterrupted coverage for policyholders, enhancing overall customer satisfaction and retention.

AI enhances every stage of the insurance business lifecycle by driving efficiency, improving decision-making, and delivering personalized experiences that meet customers’ evolving needs and expectations. By leveraging AI technologies effectively, insurance companies can gain a competitive edge, drive growth, and build long-term customer relationships.

Use cases of AI in insurance

The use case of AI in insurance includes:

Customer sentiment analysis: AI works as a powerful tool for insurers looking to enhance customer satisfaction and loyalty. Through AI algorithms, insurers can effectively analyze customer feedback, social media posts, and online reviews to gauge sentiment. By integrating sentiment analysis, insurers can gain valuable insights into customer perceptions, identifying areas for improvement and tailoring their marketing and communication strategies accordingly.

Sentiment-based marketing enables insurers to deliver targeted messages and personalized offers to customers based on their sentiments. By understanding customer sentiment, insurers can craft messaging that resonates with their audience, fostering positive experiences and strengthening brand loyalty.

Data analytics: AI plays a crucial role in business intelligence for insurers. With advanced analytics capabilities and AI integration, insurers can extract valuable insights from their data. This includes identifying trends, patterns, and correlations to inform strategic decision-making. Insurers can analyze sales performance, identify market segments, optimize pricing strategies, and enhance customer segmentation for more effective marketing campaigns.

Customer retention and relationship management: Identifying and addressing customer churn risk is critical to insurance business operations. Through AI-powered predictive modeling, insurers can effectively pinpoint customers at risk of leaving. By analyzing historical data and customer behaviors, insurers gain insights to engage with these at-risk customers proactively. This allows for personalizing retention strategies and delivering tailored experiences to improve customer loyalty and minimize attrition rates. This proactive approach strengthens customer relationships and elevates retention efforts, contributing to long-term business success.

Insurance product recommendations: Machine learning plays a crucial role in insurance by providing personalized product and policy recommendations based on extensive analysis of historical data encompassing customer behavior, demographics, and risk profiles. A prominent technique used for such recommendations is collaborative filtering. By leveraging collaborative filtering, the machine learning system can recommend life insurance to customers if their risk profile and purchasing history align with another customer who recently purchased life insurance. This approach ensures that recommendations are tailored to individual needs and preferences, enhancing customer experience and satisfaction.

Lapse management: In insurance, “lapse management” involves identifying and overseeing policies that may expire or terminate due to unpaid premiums. This process includes locating clients who are likely to lapse. Machine learning (ML) can greatly enhance insurance lapse management by helping insurers identify customers at risk of lapsing and taking necessary measures to prevent it. Additionally, ML can aid companies in segmenting customers according to their lapse risk.

Next Best Offer (NBO): A predictive analytics technique is used to determine the most suitable product or service to offer a customer based on their specific needs and preferences. In the insurance sector, NBO suggests additional insurance products to customers with a policy.

Machine learning is crucial in analyzing vast datasets to discern patterns and preferences that can inform targeted offers. For example, ML and AI algorithms can sift through customer data to identify individuals who may be in the market for a new insurance policy, such as those who have recently acquired a home or changed jobs. By leveraging these insights, insurers can tailor their offers to meet their customers’ evolving needs, ultimately enhancing customer satisfaction and retention.

Virtual assistants: Machine learning-driven virtual assistants and chatbots are prevalent in the insurance industry. These AI-powered tools use NLP algorithms to comprehend customer inquiries and provide accurate responses. These AI-powered tools continuously refine their understanding over time by analyzing extensive datasets, improving customer service efficiency and accuracy. As a common application, Chatbots leverage machine learning to interpret queries, learn from interactions, and deliver prompt solutions, ultimately enhancing customer satisfaction and reducing the workload on human agents.

Property damage analysis: Inspection marks the initial phase in processing damage insurance claims, encompassing various assets like mobile phones, automobiles, or properties. Calculating repair costs poses a significant challenge for insurers due to manual processes. AI-driven object detection technology facilitates data analysis, comparing pre- and post-incident damage levels. Machine learning models excel in recognizing damaged vehicle components, aiding in repair cost estimation. According to a PwC report, leveraging drone and AI technologies in the insurance sector could yield savings of up to US$6.8 billion annually. By harnessing drones with automated object detection, claim resolution time can be reduced by 25% to 50%.

Customer segmentation: Customer segmentation is pivotal for personalized marketing strategies, optimizing budget allocation, product design, promotions, and ultimately enhancing customer satisfaction. Machine learning tools delve into customer data to uncover insights and patterns, enabling precise identification of customer segments. AI-assisted tools streamline this process, which would otherwise be complex and laborious using manual or traditional analytical methods.

Claim volume forecasting: Forecasting claim volume is crucial to insurance operations, especially when setting premiums for the upcoming year. Machine learning plays a vital role in improving the accuracy and efficiency of this forecast by analyzing historical data to predict individual claim occurrences and total claim amounts. By prioritizing claims with higher potential impact and settling smaller, more certain claims faster, insurers can simultaneously enhance pricing precision and customer experience, ultimately improving overall business performance.

Customer lifetime value prediction: Predicting customer lifetime value (LTV) is crucial for companies seeking to optimize customer relationships, and machine learning plays a pivotal role in this process. By analyzing a customer’s purchase history, machine learning algorithms can uncover hidden patterns and group similar products together, enhancing personalized recommendations. This, in turn, encourages further purchases, thereby increasing customer retention and profitability. Understanding LTV allows insurers to strike the right balance between retaining existing customers and acquiring new ones, ultimately driving sustainable growth and maximizing profitability.

Types of models used in building enterprise AI solutions for insurance

In building enterprise AI solutions for insurance, various types of models play crucial roles in addressing specific challenges and tasks within the industry. These models are tailored to extract insights, automate processes, and make data-driven decisions. Here are some types of models commonly used:

- Underwriting automation models: Underwriting automation models utilize machine learning algorithms to streamline and automate the underwriting process. These models analyze applicant information, such as demographics, medical history, and financial data, to assess risk and make real-time underwriting decisions. For example, the decision tree can classify applicants into risk categories based on various attributes such as age, occupation, and health status.

- Pricing prediction models: Pricing prediction models leverage predictive analytics and statistical techniques to forecast insurance premiums accurately. These models analyze various risk factors, claim history, market trends, and competitor pricing to determine optimal premium rates for insurance policies. By incorporating advanced data analytics, insurers can offer competitive pricing while maintaining profitability and risk management objectives. For example, Bayesian regression models incorporate market trends and competitor pricing data for dynamic pricing adjustments.

- Fraud detection models: Fraud detection models employ machine learning algorithms to identify suspicious patterns, anomalies, and fraudulent activities in insurance claims data. These models analyze claim information, including claimant behavior, medical billing records, and transactional data, to detect fraudulent behavior and mitigate financial losses. By proactively detecting and preventing fraud, insurers can protect their bottom line, reduce claim processing costs, and maintain policyholder trust. For example, anomaly detection algorithms like isolation forests identify outliers in claim transactions that may signal potential fraud.

- Anomaly detection models: Anomaly detection models identify unusual or irregular patterns in insurance data that deviate from expected norms. These models use statistical analysis, pattern recognition, and machine learning algorithms to detect claims, underwriting applications, or financial transaction anomalies. By flagging abnormal activities or data points, insurers can investigate potential risks, errors, or fraudulent behavior, mitigating operational and financial impacts. One such example is DBSCAN (Density-Based Spatial Clustering of Applications with Noise) detects outliers as points that are not part of any dense cluster, useful for identifying irregular patterns in large datasets.

- Churn reduction models: Churn reduction models utilize predictive analytics and machine learning algorithms to identify policyholders at risk of discontinuing their insurance policies. These models analyze customer behavior, satisfaction scores, and engagement metrics to predict churn likelihood and proactively intervene with targeted retention strategies. By reducing customer attrition rates, insurers can improve customer retention, lifetime value, and profitability. Random forest classifiers can segment policyholders into high-risk churn groups and target retention efforts more effectively.

- Loss reserving models: Loss reserving models estimate the amount of money insurers need to set aside to cover future claim payments. These models use historical claims data, statistical techniques, and actuarial methods to project the ultimate cost of outstanding claims, ensuring financial stability and compliance with regulatory requirements. Markov chain models simulate future claim scenarios and estimate reserves under different loss distribution assumptions.

- Catastrophe risk models: Catastrophe risk models assess the potential impact of natural disasters and catastrophic events on insurance portfolios. These models incorporate data on historical events, geographic factors, and climate patterns to quantify the likelihood and severity of catastrophic losses, guiding insurers in managing and diversifying their risk exposure. Probabilistic catastrophe models integrate data on historical events, geographical exposure, and climate variables to estimate potential losses from natural disasters.

- Health risk assessment models: Health risk assessment models evaluate the health status and insurance risk of individuals or groups based on medical history, demographics, lifestyle factors, and genetic information. These models assist health insurers in pricing policies, determining coverage eligibility, and developing targeted wellness programs. Long short-term memory (LSTM) networks for time series analysis of health data predict future health outcomes and tailor insurance offerings.

- Life expectancy models: Life expectancy models predict the probable lifespan of policyholders based on demographic factors, health indicators, and lifestyle habits. These models are essential for life insurance companies to assess mortality risk, set premium rates, and manage longevity risk within their portfolios. For example, Kaplan-Meier estimators predict survival probabilities over time based on demographic and health-related variables.

By incorporating these specialized models into their AI solutions, insurance companies can enhance risk management, improve pricing accuracy, prevent fraud, and optimize customer retention strategies, ultimately driving business growth and competitiveness in the insurance market.

Transform Insurance with Enterprise AI!

Unlock the power of enterprise AI solutions with LeewayHertz. Tailored

for insurance, crafted for success.

How to build enterprise AI solutions for insurance operations?

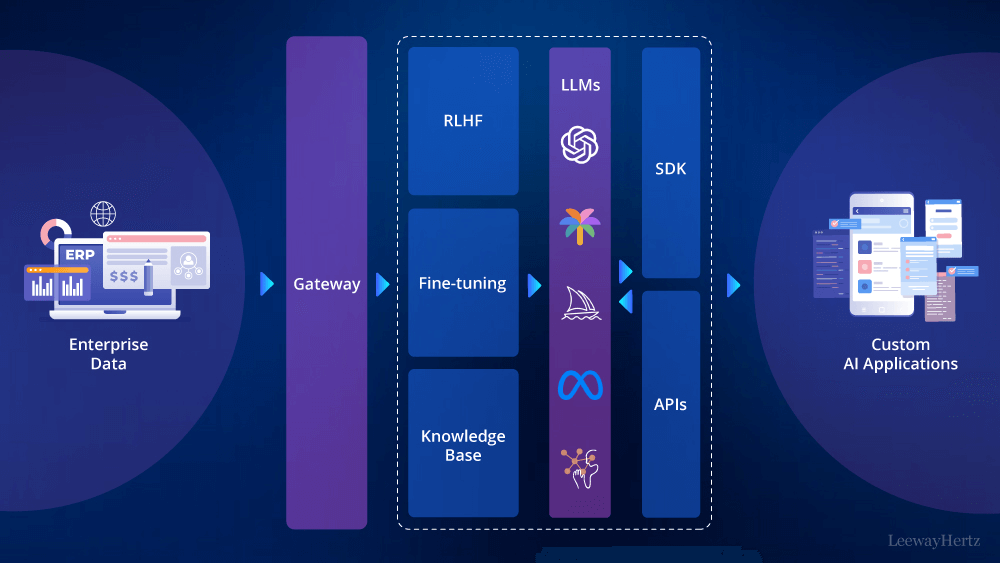

Building an enterprise AI solution in insurance involves leveraging advanced technologies to automate processes, gain insights, and make data-driven decisions within insurance companies. The integration of AI in insurance presents unprecedented opportunities for optimizing workflows and enhancing customer experiences. Developing robust enterprise AI solutions for insurance requires careful consideration of various factors, including data sources, risk assessment, and ethical considerations, to effectively leverage them in model development and decision-making processes. Now, let’s delve into the process of building an enterprise AI solution for insurance:

- The process typically begins with collecting data from internal databases, external APIs, or manual inputs. This data encompasses policyholder information, claims data, and market trends.

- Once collected, the data undergoes preprocessing to ensure it’s clean, organized, and ready for analysis.

- Next, machine learning models are developed using this processed data to address specific insurance tasks or challenges. These models are trained on historical data to recognize patterns, make predictions, or classify claims. Rigorous testing ensures the accuracy and reliability of these models before deployment.

- Once the models are trained and tested, they are deployed into the insurance organization’s existing infrastructure. This deployment phase involves integrating the models into the systems and workflows to ensure they can effectively interact with other software and processes.

- After deployment, ongoing monitoring and maintenance of the AI software are necessary to ensure its continued effectiveness. This includes monitoring the performance of the models in real-world scenarios, detecting any issues or errors, and making updates or improvements as needed. Continuous refinement ensures that the AI solution remains aligned with the evolving needs of the insurance industry, driving operational efficiency and enhancing customer experiences.

In the following section, we will delve into the development of AI-driven risk assessment and claims processing systems within the insurance sector, exploring how AI technologies are leveraged to improve efficiency, accuracy, and customer satisfaction. The objective is to assess risks, evaluate claims, and mitigate losses effectively by harnessing the power of AI algorithms and analyzing diverse data sources while adhering to ethical guidelines and regulatory requirements.

Data sources:

There can be various data sources used for data ingestion. A few of them include the following:

- Customer records and policies: Client-specific insurance policies and claims history, which are always updated, provide insurers with detailed information on individual policyholders, their coverage, and past claim experiences.

- External data sources: External data impacting insurance claims, such as weather conditions and accident reports, are sourced from real-time or historical data sources. These include weather forecasts, traffic reports, and accident databases, enabling insurers to assess external risks and adjust policies accordingly.

- Medical records and reports: Medical data relevant to health insurance claims, sourced from medical providers and databases, provides insurers with information on policyholders’ health status and medical history, assisting in processing health insurance claims accurately.

- Policyholder information: Data on insured parties, including personal and contact details, are continuously updated to ensure insurers have current information on policyholders, facilitating effective communication and policy management.

- Government and regulatory data: Data related to government regulations and taxation affecting insurance claims are sourced from government agencies such as the Department of Motor Vehicles (DMV) and the Internal Revenue Service (IRS) etc. This data covers the current and last fiscal years, providing insights into regulatory changes and tax implications on insurance operations.

These diverse data sources enable insurers to gain comprehensive insights into customer behavior, external risks, and regulatory requirements, facilitating accurate risk assessment, pricing, and claims processing while ensuring compliance with applicable laws and regulations.

Data ingestion and pre-processing:

Data cleaning:

- Data from submitted insurance claim forms and supporting documents are ingested in batches. Relevant information such as policyholder details, incident descriptions, damage assessments, and medical reports is extracted for further processing.

- Historical data related to insurance claims, including claim forms, adjuster reports, policy documents, and claimant information, are imported and processed in batches. This data provides insights into past claim patterns, amounts, and resolution outcomes.

Data pipeline:

There are several steps to ingest and pre-process data after data collection, which include:

- ETL processes: In building enterprise AI solutions for insurance, ETL includes extracting relevant information from sources such as claim forms, policy documents, and external databases, converting it into a standardized format, and loading it into the data processing pipeline.

- Data quality checks: AI can significantly contribute to implementing robust quality checks, which are essential for maintaining data integrity and accuracy in claim information, thereby ensuring reliability. This involves systematic procedures for identifying and handling missing or inconsistent data, thereby ensuring the completeness and correctness of all claims. By establishing stringent validation measures, businesses can uphold the reliability and trustworthiness of their data, crucial for decision-making and operational excellence.

Data standardization and normalization:

Standardizing and normalizing data attributes such as claim amounts, dates, and policy details ensures consistency and comparability across different claims. Companies can streamline data management processes and facilitate accurate analysis by applying uniform formats and conventions. This ensures that disparate data sets can be effectively compared and analyzed, enabling insurers to derive meaningful insights and make informed decisions. Standardization enhances data integrity and reliability, laying a foundation for more robust risk assessments and improved operational efficiency within insurance operations.

Data labeling:

Assigning labels to historical data, such as claim outcomes (e.g., approved, denied, settled), serves as the ground truth for training and evaluating the claim processing model within insurance operations. These labels provide essential context and reference points, allowing AI algorithms to learn from past decisions and outcomes. By leveraging this historical data, claim processing models can be trained to accurately predict future claim outcomes, optimize decision-making processes, and improve overall efficiency. Additionally, using labeled data helps evaluate the performance of their claim processing models, ensuring they meet predefined criteria and deliver the desired outcomes consistently.

Data structuring:

Organizing claim-related data into structured formats like relational databases enhances the efficiency of storing, retrieving, and analyzing claim information within insurance operations. These structured formats provide a systematic framework for organizing and storing data, allowing insurers to access and manipulate information as needed easily. By centralizing claim data in structured formats, insurers can streamline workflows, improve data integrity, and enable more accurate analysis. This facilitates informed decision-making processes, enhances operational efficiency, and improves customer service and satisfaction within the insurance industry.

Feature selection:

Identifying relevant features from claim data that influence claim processing outcomes, including claim type, severity, policy coverage, and claimant demographics, is critical within insurance operations. By discerning these key factors, insurers can better understand the determinants of claim outcomes and tailor their processing procedures accordingly.

Data lake:

- Raw data storage: Raw data from claim forms, policy documents, adjuster reports, and external sources is stored in a data lake for archival and analytical purposes. This centralized repository facilitates efficient data management and comprehensive analysis, enhancing insights and decision-making capabilities for stakeholders.

- Feature engineering: Deriving features or variables from raw claim data, such as claim frequency, severity trends, and fraud indicators, can significantly bolster the predictive capabilities of the claim processing model. These enhanced attributes empower the model to anticipate better and mitigate risks, ultimately improving overall efficiency and accuracy in claims assessment and processing.

Data catalog:

Establishing a metadata repository to oversee and document insurance claim data attributes streamlines navigation and comprehension of the data landscape. This organized framework enhances accessibility and ensures clarity, aiding stakeholders in effectively leveraging the wealth of information for informed decision-making and operational insights.

Data catalogs serve as essential resources for insurance professionals. They enable efficient search and retrieval of claim-related information, promote collaboration, and ensure compliance with regulatory requirements within the insurance claims processing system.

Model development

During the “development” stage of an insurance solution, data scientists focus on selecting appropriate algorithms and methodologies to build models customized to address specific industry challenges. In insurance claims processing, this stage involves selecting machine learning models suitable for classification tasks, such as determining claim approval or denial, and regression tasks, such as predicting claim amounts or settlement probabilities.

In the “Build” stage, data scientists leverage the processed insurance data to develop predictive models and algorithms to enhance the efficiency and accuracy of claims processing. This stage involves several key steps:

Algorithm selection:

In the insurance domain, data scientists may consider a variety of algorithms to address different aspects of claims processing. Classification algorithms like decision trees, random forests, logistic regression, or gradient boosting may be utilized to assess claim outcomes, such as approval or denial, based on various factors.

Regression algorithms, such as linear regression, generalized linear models, or ensemble methods, can be employed to predict claim amounts or estimate settlement probabilities. These models are trained to forecast numerical values representing the expected costs or probabilities associated with insurance claims.

Data splitting/segregation:

Historical insurance claims data is typically divided into training and validation (or test) sets during model development. Most of the data is used to train the predictive models, while a smaller portion is set aside to evaluate model performance.

This segregation allows data scientists to assess how well the developed models generalize to new insurance claims scenarios and ensures robust performance in real-world applications. By validating against unseen data, insurers can have confidence in the predictive capabilities of their models and make more informed decisions in claims processing.

Training the model:

- Input data: The pre-processed insurance data is fed into the selected algorithm for training. The algorithm learns patterns and relationships between input features, such as policyholder information, claim details, historical data, and the claim outcomes, indicating whether a claim was approved or denied.

- Loss function: During training, the model minimizes a loss function that quantifies the disparity between its predictions and claim outcomes. This involves adjusting internal parameters to improve the accuracy of claim predictions, ensuring the model aligns closely with observed insurance claim patterns.

- Hyperparameter tuning: Data scientists fine-tune hyperparameters, configurable settings of the chosen algorithm, to optimize its performance on the validation set. Techniques like grid or randomized search may be employed to systematically explore different parameter combinations, enhancing the model’s ability to generalize and accurately predict claim outcomes across various insurance scenarios.

Model testing

Once the insurance model has been trained and validated, it undergoes testing using an independent dataset.

The testing process evaluates the model’s ability to generalize to new data and estimates its performance across diverse insurance claim scenarios.

Various performance metrics are calculated on the testing dataset to assess the model’s effectiveness. These metrics may include accuracy, precision, recall, F1 score, and confusion matrix.

Selecting metrics depends on the goals of the insurance claims processing model. The trade-off between precision and recall gains significance—minimizing false positives (incorrect claim approvals) or false negatives (missed legitimate claims). The testing phase ensures the model performs robustly in real-world insurance claim scenarios, contributing to efficient and accurate claims processing.

User Interface (UI) development:

Initial UI design: Concurrently with developing the insurance model, an initial user interface is designed. This interface is tailored for end-users within the insurance environment, such as claims adjusters or underwriters, to interact with the claims assessment models.

Displaying results: The UI may include features such as displaying claim processing outcomes (approved or denied), visual representations of key factors influencing the decision, and any additional information necessary for transparency in the insurance claims processing workflow. This user interface acts as a front-end tool to facilitate effective communication and decision-making based on the predictions and insights provided by the claims assessment models.

Integration with decision workflow:

Connecting models to UI: The trained models are seamlessly integrated into the insurance system to establish a smooth data flow between the interface and the models. The UI serves as the front-end tool for interacting with the insurance analytics system, allowing end-users to input data, receive real-time predictions, and interact with the insights generated by the models, thereby enhancing the efficiency and accuracy of various insurance workflows.

Decision outputs: The outcomes of the insurance analytics system, derived from the models, are communicated through the UI.

The “development” stage is often iterative. Feedback from model performance, user interactions, and evolving business needs may lead to adjustments in the claims assessment models and the user interface. This iterative approach ensures continuous refinement, responsiveness to changing conditions, and optimization of the claims processing system for enhanced decision-making in the insurance domain.

Deployment

The deployment process of an insurance analytics model involves several key steps, leveraging containerization, Kubernetes, microservices, APIs, and a consumption layer.

Initially, the model, its code, and dependencies are packaged into a container using Docker. This containerization ensures the model’s isolation and consistent deployment across various insurance environments.

Subsequently, Kubernetes is utilized to deploy and scale the containerized of the model. Kubernetes facilitates automatic scaling based on demand, ensuring optimal resource utilization, and provides monitoring tools for tracking metrics like resource usage, response times, and error rates.

The analytics model is implemented as a microservice, enabling it to operate independently within the broader architecture. The microservices architecture streamlines the management and updating of the model without affecting other system components.

The microservice exposes well-defined APIs serving as an external interface. These APIs can be leveraged by other systems, for example, with claims processing applications, to request assessments of insurance claims. This approach promotes reusability and seamless integration with various applications within the insurance organization.

The consumption layer exposes the results of the insurance analytics model. This layer includes user interfaces for manual reviews, APIs for integration with other applications, and process interfaces that trigger downstream insurance claim processes based on claim decisions.

Deploying an insurance analytics model involves transitioning the trained model from a development environment to a production environment where it can effectively predict outcomes for new insurance claims.

Monitoring

- Model performance metrics: AI aids in implementing monitoring mechanisms to track model performance metrics, including accuracy, precision, recall, and F1 score, ensuring ongoing evaluation and optimization of the model’s effectiveness. This proactive approach enables timely adjustments and enhancements, fostering continuous improvement and reliability in claim processing outcomes. These metrics provide insights into the effectiveness of the claims assessment model in accurately predicting and classifying insurance claim outcomes.

- Data drift detection: AI can monitor the incoming insurance claims data for drift to ensure that the claims assessment model remains relevant to the evolving data distribution. Sudden changes in the characteristics of incoming data indicate a need for model retraining to maintain its accuracy and effectiveness in predicting claim outcomes.

- Error logging: AI aids in logging errors and exceptions that are crucial to identifying and addressing issues promptly within the insurance system. This includes recording discrepancies between the expected and actual model outputs and facilitating quick diagnosis and resolution of potential issues to uphold the reliability of the claims processing process.

Logging and auditing:

Audit trails: AI can maintain comprehensive audit trails for insurance analytics conducted by the model, which includes timestamps, input data, and decisions, ensuring transparency and accountability throughout the process. These detailed records facilitate traceability and compliance and enable thorough analysis and validation of outcomes, fostering trust and confidence in the analytics framework. This is crucial for compliance with regulatory standards and retrospective analysis to understand the history of claim evaluations.

Logging changes: AI aids in recording changes to the model, code, or configurations within the insurance claims assessment system is imperative for ensuring transparency and accountability. This practice facilitates comprehensive documentation of updates and modifications, enabling thorough analysis and validation of system evolution while supporting regulatory compliance and audit requirements. This practice ensures traceability and aids in understanding the context if issues arise, providing a comprehensive view of the evolution of the claims processing system.

Alerting and notifications:

Alerts for anomalies: It is vital to implement alerting mechanisms to promptly notify relevant stakeholders of anomalies or issues with the model’s performance in insurance claims assessment. These mechanisms ensure timely intervention and resolution, minimizing potential risks and optimizing the efficiency and reliability of the claims assessment process. Timely alerts help address potential problems promptly and maintain the integrity of the claims processing process.

Threshold monitoring: Setting thresholds for key performance indicators and continuously monitoring these thresholds to trigger alerts when deviations occur. This proactive approach allows for swift responses to variations in insurance data and ensures that the claims assessment system operates within predefined performance limits.

Benefits of implementing enterprise AI solutions in insurance workflow

Building enterprise AI solutions for insurance offers numerous benefits, transforming various aspects of operations and enhancing overall efficiency, effectiveness, and customer experience. Some of the key benefits of enterprise AI solutions in insurance include:

- Improved risk assessment: AI algorithms can analyze vast amounts of data from diverse sources to assess policyholders’ risk profiles accurately. This enables insurers to offer personalized policies, adjust premiums based on individual risk factors, and better manage overall risk exposure.

- Enhanced fraud detection: AI-powered fraud detection systems can analyze patterns and anomalies in insurance claims data to identify potentially fraudulent activities. By flagging suspicious claims in real-time, insurers can mitigate losses, reduce fraudulent payouts, and protect their bottom line.

- Streamlined claims processing: AI streamlines the claims processing workflow by automating repetitive tasks, like data entry and document processing. This accelerates claims processing times, reduces administrative costs, and improves customer satisfaction by providing faster claim resolutions.

- Predictive analytics: AI enables insurers to leverage predictive analytics to anticipate future trends, such as claim frequency and severity, market fluctuations, and customer behavior. This helps insurers make data-driven decisions, optimize pricing strategies, and proactively manage risks.

- Personalized customer experience: AI-powered insurance chatbots and virtual assistants enable insurance companies to deliver personalized customer experiences by providing instant support, answering queries, and guiding customers through the insurance purchasing process. This enhances customer engagement, improves satisfaction and strengthens brand loyalty.

- Underwriting automation: AI automates underwriting processes by analyzing applicant data, assessing risk factors, and determining policy eligibility in real-time. This reduces manual intervention, speeds up policy issuance and enhances underwriting accuracy, leading to more efficient operations and improved profitability.

- Operational efficiency: AI-driven automation streamlines various operational tasks, such as data processing, document management, and customer service, reducing manual effort and increasing overall efficiency. It enables insurers to optimize resource allocation, prioritize strategic initiatives, and foster business expansion.

AI holds immense potential to transform the insurance industry by optimizing processes, improving decision-making, and delivering superior customer experiences, ultimately driving competitive advantage and long-term success.

Transform Insurance with Enterprise AI!

Unlock the power of enterprise AI solutions with LeewayHertz. Tailored

for insurance, crafted for success.

How does LeewayHertz aid in integrating AI solutions into your insurance workflow?

At LeewayHertz, we specialize in seamlessly incorporating cutting-edge AI solutions into your insurance operations. Our expertise in AI technologies and deep understanding of the insurance industry enable us to enhance your workflow efficiency, risk management, and customer engagement. Here’s why you should consider partnering with us:

Tailored strategy: Through consultation, LeewayHertz understands your insurance goals and requirements. We then develop enterprise AI solutions, aligning them with your needs. This tailored approach ensures that the AI implementation seamlessly integrates into your insurance workflow, enhancing operational efficiency and effectiveness.

Expert AI professionals: LeewayHertz boasts a team of skilled professionals adept in advanced AI technologies such as machine learning, NLP, and computer vision. Our experts are dedicated to delivering precise and effective enterprise AI solutions custom-tailored to meet the insurance industry’s unique challenges and requirements.

Extensive AI experience: With a wealth of experience in AI development, LeewayHertz serves as a trusted technology partner in the insurance sector. Our portfolio showcases successfully built AI solutions, ranging from recommendation systems to insurance chatbots, demonstrating the versatility and a deep understanding of varied AI technologies.

Mission-critical security: Our team diligently follows industry-leading practices to strengthen the security of your data, algorithms, and AI systems, safeguarding them against potential threats. This steadfast commitment guarantees the resilience and integrity of your AI solutions, instilling trust and confidence in innovation, particularly within the insurance domain.

End-to-end AI development: LeewayHertz follows a comprehensive development process, starting from understanding goals and progressing through solution development, rigorous testing, and refinement. The result is a meticulously crafted enterprise AI solution seamlessly integrated into your insurance operations, driving innovation and performance.

Ensuring trust: Ethical considerations and compliance in insurance practices

In the dynamic landscape of the insurance industry, ethical considerations stand as pillars shaping every interaction between insurers and policyholders. From transparency and fairness to social responsibility, ethical decision-making forms the bedrock upon which trust and integrity are built within the insurance sector. Here are some key ethical considerations and compliance that insurance companies must adhere to:

- Transparency and disclosure: Ethical decision-making in insurance begins with transparency. Insurers are ethically obligated to provide policyholders with clear and accurate information about policy terms, coverage limitations, exclusions, and pricing details. Failure to do so could lead to misunderstandings or misrepresentation, undermining the trust between the insurer and the insured.

- Fair and equitable treatment: Discrimination based on race, gender, age, or socioeconomic status is unethical and can lead to legal repercussions. Insurance professionals must treat all policyholders fairly and consistently, ensuring that claims handling is unbiased and legitimate claims are processed promptly. Any unjust denial of claims could harm the insured and tarnish the insurer’s reputation.

- Customer well-being: Ethical decision-making in insurance goes beyond mere compliance with regulations; it involves prioritizing customers’ well-being. This includes offering coverage options that suit the customer’s actual needs and financial situation and providing adequate education about policy options and their implications. Empowering customers to make informed decisions enhances their trust in the insurer and promotes long-term relationships.

- Social responsibility: Insurance companies bear a significant social responsibility to contribute to the communities they operate within. This entails promoting safety and risk reduction, supporting disaster preparedness and recovery efforts, and participating in charitable endeavors. By considering the societal impact of their practices, insurers can create value beyond profits and enhance their reputation as responsible corporate citizens.

Ethical leadership and training: Upholding ethical standards within the insurance industry requires strong leadership committed to integrity and ethical behavior. Executives and managers ought to set the standard, exhibiting ethical behavior in their dealings with both customers and employees. Ongoing training programs covering topics such as conflict of interest, data privacy, and handling sensitive information can equip insurance professionals with the necessary skills to navigate ethical challenges effectively.

Ethical decision-making in the insurance industry is essential for maintaining trust, ensuring fair treatment of policyholders, and fulfilling broader societal responsibilities. Compliance with ethical principles not only fosters a positive reputation for insurers but also contributes to the overall stability and integrity of the industry.

Endnote

Enterprise AI solutions for insurance are indispensable for transforming every aspect of their operations. Insurance companies gain unparalleled insights into customer behavior, market trends, and risk profiles by leveraging AI-driven algorithms and data analytics. This enables them to develop personalized products, streamline processes, and optimize resource allocation. Moreover, AI facilitates proactive customer engagement, targeted marketing, and personalized retention strategies, fostering long-term relationships and maximizing customer lifetime value. In a competitive industry where innovation is key, building enterprise AI solutions for insurance empowers insurers to stay ahead, drive growth, and deliver exceptional customer experiences.

Transform your insurance business with AI: leverage the power of enterprise AI solutions tailored to your needs. Connect with our expert team at LeewayHertz today and elevate your insurance operations to new heights.

Author’s Bio

Akash's ability to build enterprise-grade technology solutions has attracted over 30 Fortune 500 companies, including Siemens, 3M, P&G and Hershey’s.

Akash is an early adopter of new technology, a passionate technology enthusiast, and an investor in AI and IoT startups.

Related Services

Enterprise AI Development

Transform ideas into market-leading innovations with our Enterprise AI services. Partner with us for a smarter, future-ready business.

Explore ServiceStart a conversation by filling the form

All information will be kept confidential.

Insights

Generative AI for startups: Empowering startups with generative AI’s potential

With Generative AI, startups can infuse their products and services with fresh ideas, captivating their clients and setting themselves apart in a crowded market.

Exploring the top use cases of AI in retail

AI has reshaped the retail industry by offering advanced capabilities like personalized recommendations, virtual assistants, and predictive analytics. Retailers use AI to analyze customer data, enabling personalized shopping experiences.

Predicting market dynamics: The rise of AI in demand forecasting

At its core, demand forecasting offers businesses a glimpse into the future, a predictive analysis that allows them to tap into consumer trends even before they fully manifest.